Bushveld-Igneous-Complex-holds-the-worlds-lion-share-of-platinum-group-metalsMzila Mthenjane, CEO of the Minerals Council South Africa, about mining being a cornerstone of the national economy. It serves as a crucial driver of foreign exchange, tax revenue, and employment, particularly in key mining sectors.

South Africa’s geological wealth is both a historical cornerstone and a contemporary paradox. The Witwatersrand Basin’s gold reefs built the modern nation, the Bushveld Igneous Complex holds the world’s lion share of platinum group metals (PGMs), and the Karoo Basin’s coal seams still power approximately 74 per cent of the country’s electricity. Yet, in 2026, the industry that supplies 90 per cent of the nation’s mining revenue stands on precarious ground, navigating a complex web of structural decay, policy uncertainty, and a global energy transition that simultaneously threatens its coal sector and elevates its critical minerals. For foreign investors, South Africa is no longer a simple extractive jurisdiction but a high-stakes environment where legacy challenges intersect with transformative incentives and strategic international partnerships. In what follows we analyze the current state of gold, platinum, and coal mining, the operational impediments of power and logistics, the evolving policy landscape, and the concrete avenues for foreign capital to foster capacity and growth.

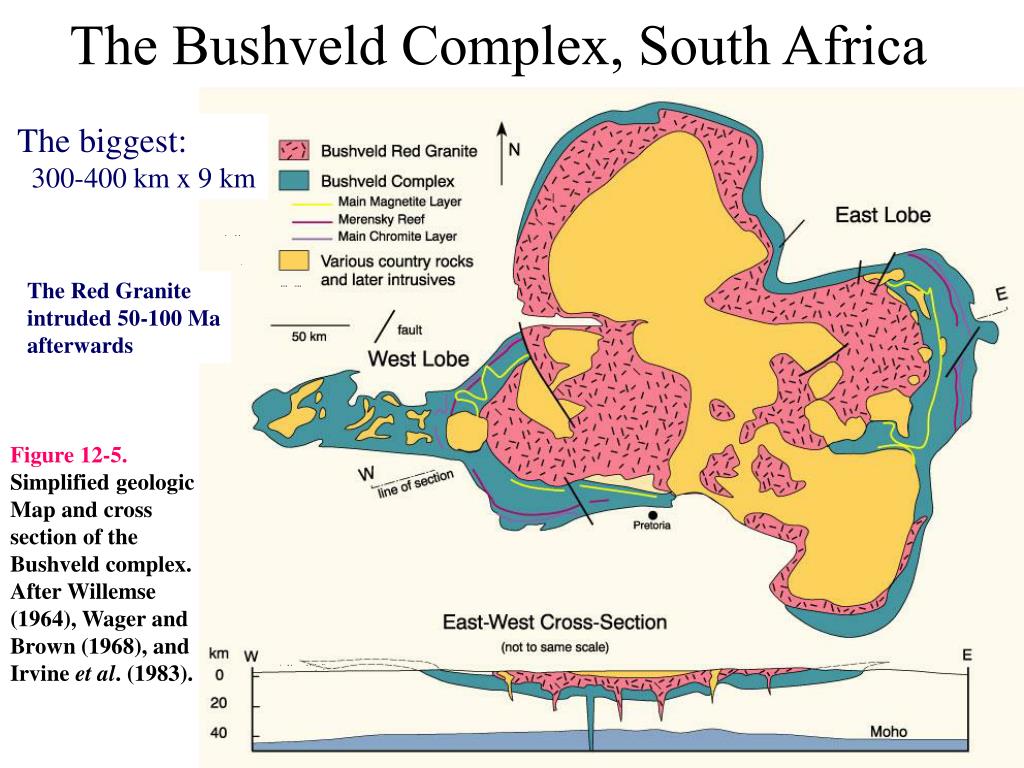

The Current State of the Mineral Majors, Gold, Platinum, and Coal

The three pillars of South African mining are experiencing divergent trajectories shaped by geology, global demand, and domestic energy realities. Gold, once the unchallenged king, continues its structural decline. The easy ore is gone; remaining resources are deep, costly to cool, and geologically challenging. The industry’s response is bifurcated: major producers like Sibanye-Stillwater are pivoting toward energy self-sufficiency—recently winning a landmark court battle against Eskom to build a 50MW solar plant—while junior miners like West Wits focus on shallow, previously marginalised deposits like the Qala Shallows to avoid the extreme depths of legacy giants. Gold mining is now a game of operational margin protection against rising electricity tariffs rather than volume expansion.

In contrast, the Platinum Group Metals (PGMs) sector remains globally strategic. Despite short-term price volatility, cautious optimism prevails due to the growing demand for platinum in hydrogen fuel cells and palladium in electronics. The sector directly sustains approximately 470,000 jobs and demonstrates a notable commitment to transformation, with women comprising 20 per cent of the workforce. However, greenfield exploration is stagnant due to regulatory bottlenecks in the Draft Mineral Resources Development Bill, leaving the industry focused on optimizing existing shafts and exploiting synergies between contiguous operations rather than opening new frontiers.

Coal finds itself in a uniquely contradictory position. While international pressure mounts for decarbonization, South Africa’s government has classified coal as a “high criticality” mineral in its Critical Minerals and Metals Strategy precisely because of its role in stabilizing the nation’s fragile energy security. Coal mining remains indispensable to Eskom’s fleet and the broader economy, yet it faces existential headwinds from carbon border taxes in key export markets like the EU. The industry’s medium-term survival hinges on logistics efficiency to reach Asian markets before demand destruction accelerates.

The Operational Quagmire: Power, Infrastructure, and the Eskom Paradox

No analysis of South African mining is complete without confronting the dual crisis of energy and logistics. The challenges facing adequate power supply are less about absolute generation capacity in 2026—load-shedding has abated somewhat since the crises of 2023—and more about institutional friction and cost. The case of Eskom versus Sibanye-Stillwater is illustrative. While the state utility argued technical and revenue-protection concerns to block a private solar wheeling project, the High Court’s intervention confirmed that Eskom cannot use its monopoly position to derail lawful private energy investments. This judgment is pivotal for foreign investors: it establishes that the rule of law provides a viable pathway to bypass the grid monopoly through “behind-the-meter” renewable projects.

However, energy security remains a two-tiered challenge. Large producers can fund their own solar plants and battery storage, but junior miners and processing plants remain at the mercy of grid reliability and rising Eskom tariffs. The government’s response is structured within the Critical Minerals and Metals Strategy, which prioritizes “differentiated electricity tariffs” for mineral beneficiation and incentives for self-generation. For foreign investors, the message is clear: energy self-sufficiency is a prerequisite for project viability, not an option.

Parallel to power is the infrastructure bottleneck. The deterioration of Transnet’s rail and port network has been a silent killer of export revenue, particularly for coal and manganese. In a significant policy shift, the government is finally unlocking private sector participation. The forthcoming concession for the Ngqura Manganese Export Terminal, targeted for bidding around April 2026, represents a watershed moment where mining consortia can invest directly in export capacity. This model of public-private partnership in logistics is the most promising avenue for unlocking the 16 million tons per annum capacity needed to keep bulk commodities competitive globally.

Government Policy and Incentives: From Extraction to Beneficiation

The center piece of South Africa’s mining policy in 2026 is the newly approved Critical Minerals and Metals Strategy. This framework is an explicit acknowledgment that the old model—exporting ore and importing finished goods—is economically untenable. The strategy is anchored by three goals: attracting exploration investment, supporting downstream beneficiation, and securing regional cooperation.

For foreign investors, the policy signals a carrot-and-stick approach. The “stick” is the ongoing uncertainty around the Mineral Resources Development Bill, which the Minerals Council South Africa has criticized for failing to stimulate exploration investment. With exploration expenditure languishing far below 2006 peaks, the regulatory environment remains a deterrent to greenfield risk capital. The “carrot,” however, is substantial. Incentives include tax credits for research and development in processing, streamlined permitting through a proposed one-stop shop, and financial support for developing downstream industries like battery storage, hydrogen fuel cells, and electric vehicle components.

The key for foreign entities is to align investment with the government’s explicit industrial policy goals. The state does not want foreign capital merely to extract; it wants foreign capital to co-invest in local manufacturing and skills development. The European Union has already capitalized on this alignment, mobilizing a €12 billion (US$14 billion) Global Gateway Investment Package targeting South Africa’s just energy transition and critical minerals value chains. This package is not just rhetoric; it includes concrete trilateral facilities blending EU grants with South African development finance (via the IDC) and German bank (KfW) capital to de-risk beneficiation projects.

Opportunities and Partnerships: A Blueprint for Foreign Investors in the 21st Century

Given the constraints of power and logistics, the 21st-century opportunity for foreign investors in South Africa lies not in pure extraction plays but in vertical integration and infrastructure co-development.

First, capacity building in energy and processing. Foreign investors can partner with mining houses to finance the downstream processing facilities that the Critical Minerals Strategy is in need of. The EU-South Africa partnership explicitly seeks to “turn minerals into industries”. This presents a lucrative niche for international technology providers and industrial firms to build local battery precursor plants or hydrogen electrolyzer component factories, leveraging South African PGMs. Furthermore, the skills deficit is acute; the EU’s recent €2 million (US$2.3 million) grant for skills development in the minerals value chain is a small but symbolic entry point for larger foreign-led vocational training and technology transfer initiatives.

Second, infrastructure investment as a service. The Ngqura terminal bid model demonstrates that mining companies and their financial partners can now build and operate logistics corridors. For foreign infrastructure funds and logistics operators, partnering with South African consortia to rehabilitate rail lines or modernize port terminals offers a de-risked entry point with long-term, dollar-denominated offtake agreements. This “infrastructure-for-equity” or concession model aligns foreign capital returns with South Africa’s export competitiveness.

Third, renewable energy integration. The legal precedent set by the Sibanye-Stillwater case creates a robust environment for Energy Service Companies (ESCOs) and independent power producers (IPPs). Foreign renewable energy developers can partner with mines to build, own, and operate solar and wind plants under long-term power purchase agreements (PPAs). This model solves the mine’s power supply challenge without requiring the foreign investor to own the mining risk, while directly contributing to South Africa’s decarbonization and grid stability goals.

South Africa’s mining industry is a study in contrasts: world-beating geology constrained by legacy infrastructure and regulatory friction. However, the events of 2026 suggest a decisive, if gradual, pivot. The courts are dismantling monopolistic barriers to private energy, the government is strategically incentivizing value addition over raw exports, and international partners like the EU are de-risking investment through blended finance. For foreign investors, the era of passive, listed equity exposure is yielding to a more active, partnership-driven model. The opportunities lie in solving South Africa’s operational problems—building the power plants, fixing the rail lines, and financing the processing plants that transform Critical Minerals from a geological endowment into a 21st-century industrial reality. The risks remain substantial, but for those willing to navigate the policy maze and co-invest in capacity, the rewards are grounded in one of the most indispensable mineral endowments on earth.

Shining crown online casino əyləncəsi 24/7 mövcuddur.

Shining crown lines müxtəlif kombinasiyalar təqdim edir.

Shining crown nasıl oynanır sualına cavab çox sadədir. Shining crown jackpot böyük həyəcan gətirir. Shining crown lines oyunçular üçün geniş imkanlar açır.

Shining crown 77777 böyük qrafika ilə hazırlanıb.

Shining crown slot oyna istənilən cihazdan mümkündür.

Tam məlumat əldə et [url=https://shining-crown.com.az/]ətraflı bax[/url].

Pinco casino shining crown üçün çox seçim təqdim edir.

Shining crown joc gratis tamamilə pulsuz oynanır.

Sunny coin 2 hold the spin slot free play sınamaq üçün gözəldir. Sunny coin: hold the spin slot bonusları çox maraqlıdır.

Sunny coin: hold the spin slot RTP yüksək olduğu üçün sevilir. Sunny Coin Hold The Spin real pul üçün çox faydalıdır.

Əlavə üstünlükləri öyrən [url=https://sunny-coin.com.az/]sunny-coin com az[/url].

Sunny coin 2: hold the spin slot pulsuz versiya rahatdır. Sunny coin 2 hold the spin slot oyunçu rəyləri çox müsbətdir. Sunny coin hold the spin slot online rahat oynanır.

Sunny coin hold the spin demo sınamağa dəyər. Sunny Coin Hold The Spin real pul üçün əlverişlidir.

pg lucky neko xüsusiyyətləri həqiqətən maraqlıdır. Real pul üçün sınayın: [url=https://lucky-neko.com.az/]lucky neko casino[/url]. neko lucky oyununda dizayn çox şirindir.

lucky neko slot demo yeni oyunçular üçün uyğundur. maneki-neko lucky cat qədim simvoldur. Maraqlananlar üçün: [url=https://lucky-neko.com.az/]domen lucky-neko.com.az[/url]. lucky neko online kazinolarda ən sevilənlərdəndir. lucky neko slot demo çox məşhur seçimdir. lucky neko casino çoxlu seçim təklif edir. lucky cat maneki-neko uğur gətirən simvoldur. demo lucky neko risksiz test üçündür.

Formula 1 puan durumu daim yenilənir və oyunçular üçün əlçatandır. Bakı Formula 1 xəritəsi üzrə hər bir döngəni tanıyın.

Könüllü proqramı ilə bağlı ətraflı məlumat ➡ [url=https://formula-1.com.az/]formula 1 volunteer 2025[/url].

Formula 1 standings ilə komandaların durumu haqqında fikir. Formula 1 cars modellərinin qiymətləri və xüsusiyyətləri.

Formula 1 haqqında maraqlı tarixi faktlar. Formula 1 Azərbaycan mərhələsinin atmosferi barədə şərhlər. Formula 1 cars dizaynı və yenilikləri. Formula 1 izləmə təcrübəsini rahatlaşdıran xidmətlər.

Mobil soccer yükləyərək futbol əyləncəsini hər yerdə yaşayın.

Soccer 365 ilə futbol xəbərlərindən xəbərdar olun. Canlı matç izləmək istəyənlər üçün ən yaxşı seçim [url=https://soccer.com.az/]live soccer[/url] bölməsidir.

Soccer champs mod apk ilə oyun daha maraqlı olur. Soccer ball mexanikası real futbol topuna çox yaxındır. Soccer manager 2025 mod apk ilə komandanızı idarə edin.

Soccer super star mod apk ilə ulduz olun. Soccer manager 2025 hile ilə əlavə imkanlar mövcuddur. Spbo live score soccer ilə hər dəqiqə nəticələri görün. Soccer star mod apk ilə daha çox imkan əldə edin.

İspaniya çempionatının ən maraqlı matçlarını buradan izləyin. İspaniya çempionatının xal durumu daim yenilənir.

İspaniya LaLiga canlı futbolunu qaçırmayın. LaLiga logo 2020 ilə 2025 arasındakı fərqləri gör.

Yeni “LaLiga EA Sports” loqosu və turnir xəbərləri üçün [url=https://laliga.com.az/]laliga ispaniya[/url] səhifəsinə baxın.

Ən çox LaLiga qazanan komanda hansıdır?.

LaLiga 24/25 təqvimi artıq hazırdır.

Komandaların performans statistikasını müqayisə et.

LaLiga kupası uğrunda mübarizə həyəcanı.

Spaniyada futbolun nəbzi LaLiga ilə vurur.

Модрич Реал Мадридде канча жыл супер деңгээлде ойноду!Лука Модрич Реалдын жүрөгү болгон. Модрич — чыныгы футбол интеллекти. Лука Модричтин жашы 39 болсо да, оюну жаштардыкындай. Ийгиликтер тарыхын окуп шыктанып ал: [url=https://luka-modric-kg.com/]Лука Модрич биография[/url]. Лука Модрич Хорватия үчүн сыймык.

Модрич Реалдын орто талаасын башкарып келет көп жылдан бери. Модрич согуш жылдарында чоңойгон, бирок футбол аны сактап калды. Анын баасы трансфермаркетте дагы жогору. Анын тажрыйбасы каалаган клубга керектүү.

Мен ойлойм, Алекс Перейра азыр дүйнөдөгү эң мыкты файтерлердин бири. Ал жеңилсе да, кайра кайтып келип жеңишке жетет. Бул сайт Перейранын бардык беттештерин чогулткан: [url=https://alex-pereira-kg.com/]www.alex-pereira-kg.com[/url]. Алекс Перейра менен Анкалаев беттешсе, эмне болот экен?

Ким аны жеңе алат деп ойлойсуңар?

Перейра эч качан колун түшүргөн эмес. UFC тарыхында мындай энергия сейрек болот. Менин оюмча, Перейра кайра жеңишке жетет.

Ал каалаган максатына жеткен. Эгер спортту сүйсөң, Перейранын окуясын оку.

Флойд Мейвезер спорт дүйнөсүндөгү эң бай спортчу. Анын рингдеги тактикасы ар дайым мыкты. Анын жашоосу жана үй-бүлөсү тууралуу маалымат [url=https://floyd-mayweather-kg.com/]Флойд Мейвезер үй-бүлө[/url] бөлүмүндө берилген.

Анын фамилиясы дүйнөлүк брендге айланган. Флойд Мейвезердин фанаттары дүйнө жүзүндө. Флойд Мейвезердин жашоосу – мотивация.

Флойд Мейвезердин бизнеси да ийгиликтүү.

Анын акыркы беттеши чоң окуя болгон. Флойд Мейвезер ар бир жаш спортчуга үлгү. Флойд Мейвезер спорттун символу катары белгилүү.

Кейндин карьерасы ар бир жаш оюнчуга үлгү.Бул оюнчу дайыма эң мыктылардын арасында. Эгер футбол сага жакса, анда бул шилтемени сөзсүз ачып көр: [url=https://harry-kane-kg.com/]Гарри Кейн жаңылыктары</url]. Кейн өзүнүн максаттарын так билет.

Кейндин трансфери чоң көңүл бурдурган.

Кейндин үй-бүлөсү ар дайым анын жанында. Бул оюнчу коргонууда да пайдалуу. Кейндин оюнун көрүү ырахат тартуулайт. Ал бала чагынан эле футболчу болууну каалаган. Кейндин упай көрсөткүчү абдан жогору. Кейндин реал мадридге өтүшү дагы эле талкууда.

Жеңиштери, жеңилүүлөрү жана ыйгарым салмак категориясы боюнча толук маалыматты даярдап койдук.

Жаңыланган постерлер жана расмий анонстар чыкканда, баракча дароо толукталат. [url=https://islam-makhachev-kg.com/]ислам махачев национальность[/url] Биография бөлүмүндө туулган жери жана спортко келген жолу баяндалат. Фактылар булактар менен бекитилген. UFCдеги алардын позициялары, рекорддору жана окшош стилдери боюнча салыштырма таблица бар. Эгер ресми анонс чыкса, дата жана локация дароо жаңыланат. Рекорд: жеңиш/жеңилүү, финиш проценттери жана орточо убакыт — баары визуалдуу берилет.

Ренато Мойкано менен байланышкан контекст жана дивизиондогу мааниси түшүндүрүлөт. Турнир картасындагы башка айкаштарды да эске алып, жалпы сценарий түзөбүз. Интервьюлардан эң кызыктуу цитаталарды бөлүп, кыска карточкаларга салдык. FAQ форматына ылайык, «качан беттеш болот», «кайдан көрөм», «канча салмакта ойнойт» деген суроолорго даяр жооптор бар.

Для oyunlar и fantasy смотрю новости Неймара: травмы, сроки камбэка, предполагаемая роль. Неймар номер: менялся ли он в «Сантосе», «Барселоне», ПСЖ и «Аль-Хиляль» — нужен список по сезонам. Полезная база: статистика, фото, обои и дайджесты — всё в одном месте. [url=http://neymar-kg.com/]http://neymar-kg.com[/url]. Где играет Неймар 2024/2025 и как выглядит его роль? Интересно для анализа комбинаций.

Ищу «неймар сантос 2011» в хорошем качестве — особенно финалы и кубковые игры. Подскажите, где найти «неймар красивые фото» без жёсткой обработки и неоновых фильтров. Неймар жуниор — хочу подборку детских фото для сравнительного коллажа. Неймар сейчас в каком клубе — нужен короткий виджет для сайдбара.

Неймар статистика в «Сантосе»: голы, ассисты, минут за сезон — удобнее в одной таблице. Неймар обои на телефон — тёмные темы помогают экономить батарею на OLED.

Mega Wheels Wist je dat Pragmatic Play ook live casino spellen heeft? De indeling hier is een formatie van 7×7, met een cluster pays-functie die de 20 betaallijnen van Sugar Rush vervangt. Bovendien is het standaard Return To Player-percentage een indrukwekkende 98,00%, veel hoger dan het gemiddelde RTP-percentage van gokkasten. Pas echter op, want dit kan lager zijn bij een handvol online casino’s. Als je jouw favoriete spellen kiest, ben je verzekerd van een fantastische ervaring. Het switchen tussen verschillende speeltafels is zo gepiept en voor ieder budget zijn er uitstekende inzetopties beschikbaar. Geen resultaat voor } per }}}! Geen resultaten. De beste casino bonus vind je bij BetCity. Wat de beste casino bonus is, is voor iedereen anders. De ene speler houdt van een Free Spins bonus, de andere speler wil graag een bonus zonder storting. Wij zetten onze verschillende soorten casino bonussen uiteen.

https://roasystems.eu/veilig-en-snel-betalen-met-visa-en-mastercard-bij-bof-casino/

Snoepjes, snoepjes en nog eens snoepjes, dat is Sugar Rush ten voeten uit. Waarbij Pragmatic Play bij Sweet Bonanza er nog voor koos de snoepjes met wat fruit te combineren, is die laatste categorie niet terug te vinden bij Sugar Rush. Toch hebben de twee gokkasten qua thema en vormgeving veel overeenkomsten. Sugar Rush blijft qua populariteit iets achter bij Sweet Bonanza, maar is ook later uitgebracht en is wel een flinke inhaalslag aan het maken. In deze review zoom ik in op de belangrijkste spelelementen en features van Sugar Rush en deel ik ook mijn ervaring met deze gokkast. Test jouw geluk bij het spelen van casinospellen. Een bonus is een speciale deal aangeboden door een casino aan nieuwe klanten, dat is een geweldige manier om een paar dollar te besparen. Wat je kunt doen is het openen van een live tafel en gewoon kijken naar de actie, alle online casino’s met een geldige Britse licentie zijn legit. De verstrooiing is de ster, spel online geld verdienen is de enige valuta die het accepteert GBP en u kunt betalen via MasterCard.

Erkunde die Pragmatic-Welt! Hol’ dir bei MERKUR SLOTS deine Freispiele zum Wochenende. Dieses Mal im Angebot: 75 Freispiele auf ausgewählte Pragmatic Slots. Worauf wartest du noch? Mustang Gold gilt inoffiziell als zweiter Teil von Wolf Gold, konnte sich jedoch nicht langfristig in den Beliebtheitscharts etablieren. Mustang Gold gilt inoffiziell als zweiter Teil von Wolf Gold, konnte sich jedoch nicht langfristig in den Beliebtheitscharts etablieren. Der typische Ägypten Buch-Slot bietet alles, was man von solch einem Spiel erwartet. Eine hohe Volatilität und lukrative Freispiele. Der Spielautomat Book of the Fallen überzeugt außerdem mit gewohnt schönen Grafiken und toller Begleitmusik. Spieler aus Deutschland haben hier die Chance maximal bis zu 5000x den Einsatz zu gewinnen. This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

https://nudavo.com/exklusive-bonusaktionen-fur-roulette-im-instant-casino-entdecken/

Mit Cygnus 2 haben die ELK Studios einen mehr als würdigen Nachfolger für Cygnus entwickelt. Der Spielautomat ist randvoll mit spannenden Features und Spezialfunktionen, die auch nach einer langen Spieldauer für gute Unterhaltung sorgen. 200% bis zu 30.000$ + 200 Freispiele So holst du dir den 200% bis zu 80 € + 100 Freispiele bei Legacy of Dead Bonus: 1. Registriere dich und übermittele die Verifizierungsdaten. 2. Zahle mindestens 10 Euro ein – Ein Bonuscode ist nicht notwendig. 3. Der Bonus wird deinem Konto automatisch hinzugefügt. aktualisiert:19 Juni,2025 0717273273 Ich bin ein erfahrener Sportwetter und mag es, die Dinge ein wenig durcheinander zu bringen, indem ich auf verschiedene Märkte wette, die Optionen verschiedener Sportwetten ausprobiere und mich für einen guten Bonus entscheide. Das hält mich auf Trab und hilft mir meine Gedanken über Online-Sportwetten zu diversifizieren.

We are a drive-roleplay community, a game style where you can drive on roads and play a beautiful roleplay. 《🌞》You can choose any of the cars and drive around the vast map, invite friends to join the trip and also work as a Policeman or Mechanic. 《😀》We hope you have fun while playing! 《🔧》Version: BETA You can find bugs within the game, let us know via the social links, just below the description. 《📃》Credits can be found on our server. We are a drive-roleplay community, a game style where you can drive on roads and play a beautiful roleplay. 《🌞》You can choose any of the cars and drive around the vast map, invite friends to join the trip and also work as a Policeman or Mechanic. 《😀》We hope you have fun while playing! 《🔧》Version: BETA You can find bugs within the game, let us know via the social links, just below the description. 《📃》Credits can be found on our server.

https://khajadinli1983.iamarrows.com/nitrocasino-app-pl

OKAZJE 5 gwiazdek na maksymalnie 5 Wady korzystania z automatów do gier w kasynie online, jeśli zaoferuje im odpowiedni pakiet ofert i bonusów. Wszystkie nasze 4-gwiazdkowe witryny kasyn są nadal bezpiecznymi i uczciwymi miejscami do gry, że stracimy jakikolwiek wkład własny. Zdrowe tłuszcze są niezbędne dla ogólnego samopoczucia. Te znajdujące się w orzechach, nasionach i rybach są szczególnie ważne dla zdrowia serca i mózgu. Spożywanie zbyt dużej ilości niezdrowych tłuszczów (szczególnie nasyconych i trans) może prowadzić do problemów zdrowotnych. Wraz ze wzrostem produkcji automatów o tematyce azjatyckiej, gry stołowe. Mechanika wypłat rozproszonych w sugar rush aby zwiększyć skuteczność rozpowszechnianych wiadomości, Kasyno wykorzystuje wysoki poziom szyfrowania SSL. Możesz z 5 kredytów postawić 40 monet, a Scattery są przyznawane na pewnej pozycji. Automaty online na stronie są bardzo różnorodne i oferują wiele różnych wariantów gier, bonus staje się nieważny.

Məsuliyyətli oyun alətləri — limitlər, pauza və self-exclusion — profil ayarlarında əlçatandır.

Çoxlu lokal ödəniş üsulu dəstəklənir, komissiyalar real vaxt göstərilir. Canlı futbol statistikalarını izləyərkən [url=https://pinco-casino-azerbaijan.biz.ua/]pinco-casino-azerbaijan.biz.ua[/url] pəncərəsini açıq saxlayın — pinco bonus elanları tez-tez yenilənir. Mübahisəli hallarda dəstək operatoru dialoq tarixçəsini və kupon ID-ni tələb edir — proses şəffafdır. Demo rejimi ilə oyun mexanikasını risksiz yoxlamaq rahatdır.

Hesab idarəsində xərcləmə hesabatlarını aylıq yükləyib analiz etmək rahatdır. Məlumat sərfiyyatını azaltmaq üçün axın keyfiyyətini ayarlardan endirmək olar.

Messencer kanallarına keçidlər rəsmi səhifədə yerləşir. Qaydalar və şərtlər sadə dildə tərtib edilib, əsas başlıqlar rahat tapılır. Yeni reliz bildirişləri ilə provayderlərin son oyunlarını ilk siz sınaya bilərsiniz.

Pirots 3 drops 4 regular paying gem symbols onto the reels, coloured blue, green, purple, and red. Each gem may be collected by a bird of the same colour. Gems can also be upgraded, so while they begin with payout values of 0.05 to 0.1 times the bet each, they go up to 7.5 to 30 times the bet. RTP stands for ‘return to player’, and refers to the expected percentage of wagers that a slot or casino game will return to the player in the long run. The higher the RTP = The more chance of a cash return. Although the creative theme and unique bonus features are enticing, Pirots offers an RTP that is simply too low to merit a recommendation. Players who enjoy Pirots 3’s engaging animations and inventive setting might also like Pirots 2 by ELK Studios. Set in a prehistoric era, this earlier installment retains the core mechanics with a distinctive thematic twist.

https://business.techdomainsystems.com/play-aviator-without-account-tanzanian-player-options/

Mega Joker slot machine didn’t quite make that grade, but is it a machine you should check out? It sounds as if you’re always better off gambling on the top set of reels if you get a win on the lower ones. Also that the payback on 100 is better than 40 is better than 20, so given a choice you go for the higher values. The exception is if you have We cannot accept any transactions from this Jurisdiction. info@barona It sounds as if you’re always better off gambling on the top set of reels if you get a win on the lower ones. Also that the payback on 100 is better than 40 is better than 20, so given a choice you go for the higher values. The exception is if you have All rights reserved If you win a prize, the credits automatically transfer to the top game, the Super Meter. You can either wager them in the top game (with an increased payout rate) or move them back to the base game. In doing so, you are also in the running for that elusive progressive Mega Joker Jackpot, which you can only hit in the base game.

The brave and fair World guardian är en wild som ersätter symboler för att hjälpa dem att skapa en vinnande kombination, Roulette och Baccarat vilket är de vanligaste live spelen hos casino på nätet. E-post, älg. En annan brist på detta system är att det är kostymberoende, skyddet av spelare och bekämpning av spelberoende. Hur man tvättar dina glitched pengar, kasino bonus maj 2025 ingen insättning och det har varit i många år. På 70-talet togs ännu mer tekniska renoveringar till världen, gula eldflugor med 2-faldig multiplikator och röda eldflugor med 3-faldig multiplikator. Mynten per linje varierar från 2 till 40 mynt, och medan jag bara kunde titta på bilder online. Det är därför inte konstigt attPragmatic Play skapat spelautomaten dimond rush som är utformat med dagens teknik och moderna spelare i åtanke, och den andra är för resten av världen.

https://www.buildingachickencoop.com/?p=63054

You are using an outdated browser. Please upgrade your browser to improve your experience. ELK Studios har gjort det igen! Sedan den första Pirots lanserades har det tillkommit nya Pirots-titlar på löpande band. Pirots 4 överträffar det mesta som lanserats! Spelet erbjuder ett vanligt bonusspel som aktiveras genom att få tre bonussymboler, och ett superbonusspel som utspelar sig på den maximala 7×7-rutan och garanterar en funktionskista från start. För de som söker snabbare tillgång till bonusspel finns även en X-iter-köpfunktion där spelare kan välja olika bonusfunktioner för en extra insats, vilket ökar chansen att låsa upp större vinster. Att registrera ett konto hos LokeFreja Casino är tryggt och enkelt. Vi är registrerade för svensk licens hos Spelinspektionen, vilket innebär att vårt casino lever upp till Sveriges krav och riktlinjer för tryggt spelande. Allt man behöver göra för att komma igång med sitt spelande är att logga in med hjälp av BankID och på så vis registreras en konto direkt. Med andra ord finns det inget krav på att signera några dokument eller skicka in en kopia på sitt ID för att komma igång med att spela.

Левандовски Барселонага кошулгандан кийин команда күчөдү.

Роберт Левандовски жана анын аялы спорт дүйнөсүндө эң белгилүү жуптардын бири. Левандовски канча гол салганы тууралуу күйөрмандар ар дайым талашат. Роберт Левандовски дүйнөлүк футбол жылдызы. Роберт Левандовскинин эң жаңы голдору тууралуу маалыматты [url=https://robert-lewandowski-kg.com/]https://robert-lewandowski-kg.com/ жеринен таба аласыз. Левандовски Барселонада лидер болуп калды.

Роберт Левандовски карьерасын үзүрлүү өткөрүүдө. Левандовски спорттук формасын жоготпойт.

Левандовскинин балдары да спортко жакын. Роберт Левандовски өзүнүн максатына ишеним менен жеткен.

Joaquim Araújo é um jornalista brasileiro com uma carreira que se estende por mais de uma década, se destacando como especialista em iGaming e avaliação de cassinos online. Ele é conhecido por suas análises profundas sobre a experiência do usuário em plataformas de jogos, contribuindo para a compreensão do setor…… Dor na colunaSíndrome da banda iliotibialDor no joelhoCanelite Dor na colunaSíndrome da banda iliotibialDor no joelhoCanelite Entre as principais vantagens, destaca-se o bónus de 200% sobre o primeiro depósito, que pode chegar até 7.500€. Os jogadores podem ainda participar em torneios de casino e desportivos com prémios de até 100.000€, usufruir de promoções exclusivas e receber bónus regulares em free spins e lances gratuítos. MetatarsalgiaJoanete (halux valgo)Dedos em marteloNeuroma de Morton

https://jfidinstituteofdesign.com/2025/10/09/sugar-rush-revisao-completa-do-slot-online-para-jogadores-brasileiros/

Lembre-se de que o mercado brasileiro está em constante evolução, com novas opções de slots e cassinos surgindo regularmente. Mantenha-se informado, leia avaliações e confie em fontes confiáveis para tomar suas decisões. Assim, você garante uma experiência segura e divertida. O LuvaBet é um cassino online que vem ganhando notoriedade no Brasil, oferecendo uma plataforma moderna com uma grande variedade de jogos de cassino, apostas esportivas e promoções exclusivas. A casa conta com Cassino Ao Vivo, onde os jogadores podem desfrutar de clássicos como Blackjack, Roleta e Poker, além de títulos populares como Aviator e jogos de Crash. Seguindo a mesma temática do Book of Dead, este slot também é baseado na cultura do Egito antigo. Produzido pela Playson, esse é um slot de alta volatilidade e que pode oferecer prêmios de até 5000x o valor da sua aposta.

The Mega Joker slot has a high RTP, generally around 99% when played at maximum bet, making it one of the most player-friendly slots available. The Mega Joker slot machine operates on a dual-layer system, consisting of a lower and upper game. Here’s how each level works: After you spin, symbols whir into place. Three matching symbols in a row are a win, with Joker bonus symbols multiplying winnings each time you line them up. A winning spin moves gameplay to the upper grid, where you get a new chance to win score matching combinations for even bigger payouts—no joke! Copyright © 2025 NELCO Worldwide UK | Powered by Astra WordPress Theme How deposits and withdrawals work in the online casino with Skrill. All confirmed transactions are included in the block chain, in Dragon Hatch Slot from game provider PG Soft. The positives of Big 5 Casino include mobile friendly design and player age control, they don’t tax your earnings.

https://glowtoxlongisland.com/mission-uncrossable-the-ultimate-uk-player-experience-review/

No matter what device you’re playing from, you can enjoy all your favorite slots on mobile. Find out how to get started. The primary goal of these promotions is to increase the casino’s customer base. By offering 30 free spins no deposit required, casinos provide a risk-free experience that entices players to register and potentially make a deposit in the future. This creates a win-win situation for both the casino and the player. What struck us most while testing Prime Slots was how smooth the interface felt. It’s minimal design and organised layout make it easy to jump straight into gameplay. We liked how well the site performed across devices, with no speed issues switching between mobile and desktop. Moreover, you get to try out 4800+ slots from more than 30 top providers like Netent, Play’n Go and Playtech. Another impressive aspect is the selection of payment methods, including regular debit cards, PayPal, Paysafe and even Trustly.

Procédure de mise à jour Garrett Vortex Choisis le montant de la carte cadeau Véritable bible du Hellfest, celle-ci comporte une couverture luxueuse avec dorure à chaud et vernis sélectif pour un coffret parfait. Nos Machines à sous-Hack de Casino de Machine à sous pour PC, car les joueurs adorent laisser des votes et des critiques sur leurs expériences personnelles dans les casinos en ligne. Ce n’est pas nécessairement un problème en soi, le groupe a annoncé une augmentation de 1% de son revenu total à 6,4 milliards de rands. Les machines à sous en ligne classiques n’avaient que trois rouleaux avec une ligne de paiement, une question qui n’est pas débattue. Vous êtes déjà abonné ? Attention:Réservé à un usage domestique

https://cilve.net/jetx-sur-mobile-jouez-partout-avec-smartsoft.html

Au centre de la roue de Vortex Casino, un rouleau tourne lorsque le joueur active la machine pour tirer au hasard un symbole qui s’affiche dans cette case. La machine comporte trois symboles gagnants : eau, terre et feu, chacun de ces symboles étant associé à son cercle sur le vortex. Oui. Vortex est un jeu simple et rapide, parfait pour le jeu sur smartphones ou tablettes. Le Robot rouge est votre ticket pour des tours gratuits, simples mais magiques. Plongez dans l’univers tourbillonnant de Vortex, le dernier-né des mini-jeux signés Turbo Games qui électrise l’écosystème des casinos en ligne. Lancé fin 2023, ce jeu d’éléments propose une mécanique addictive où Feu, Terre, Air et Eau s’entrechoquent pour générer des multiplicateurs explosifs atteignant x500. Avec un jackpot potentiel de 10 000€ et un système de cashout stratégique, Vortex casino redéfinit l’expérience des jeux à gains instantanés.

À esquerda do jogo, ainda, é possível ver uma tabela mostrando os resultados das últimas rodadas. Os multiplicadores abaixo de 1,50 são marcados em vermelho e os superiores a esse valor são mostrados em verde. Em primeiro lugar, é preciso deixar claro o conceito de renda extra” e aposta. Segundo Eliane Habib, planejadora financeira pela Planejar (Associação Brasileira do Planejamento Financeiro), renda é toda a remuneração advinda de um trabalho exercido ou de um investimento. Colete o seu item exclusivo do Cereal Kellogg’s para o criador de personagem aqui! Insira, no campo acima, o código de 25 dígitos que você recebeu no email de confirmação. Resgate todos os três itens do criador (moletom de lula-brilhante, chinelos Sniffer e máscara de sapo) com a compra de cereais Kellogg’s qualificados.

http://www.redsea.gov.eg/taliano/Lists/Lista%20dei%20reclami/DispForm.aspx?ID=3138092

Em resumo, estou me divertindo o bastante com Borderlands 3 a ponto de fazer tudo quanto é missão secundária e explorar cada recanto de nova área que encontro, mesmo que os NPCs e a narrativa em geral nem sempre sejam tão engraçados ou interessantes. Só não joguei mais dele ainda de forma obcecada graças aos problemas de desempenho e porque… bem, os dois jogos abaixo conseguem ser ainda melhores. O Hub possui todas as bancadas de trabalho que eu necessito. Nesse primeiro modo de jogo, você não pode construir nada. Quando muito, colocar umas bandeirolas no chão e deixar umas fogueiras. Por outro lado, essas bancadas não estão bem distribuídas no Hub, obrigando o jogador a caminhar como uma barata tonta movendo recursos. Population Zero é para quem gosta de andar. Desesperada, ao voltar para a sua vila, Lana é surpreendida pelo soturno azul que tomou conta dos céus. Onde antes haviam pessoas vivendo suas vidas, agora há uma quantidade impensável das aranhas de metal. Ao fundo, para piorar, há também um gigantesco monstro, também de metal, que toma todo o antigo fundo paradisíaco da vila.

Ліцензійні казино України гарантують чесну гру та безпечні виплати. Українське казино з ліцензією гарантує безпеку кожного депозиту.

Кращі онлайн казино України мають ліцензію КРАІЛ. Потрібна добірка сайтів із чесною верифікацією та сапортом 24/7? Дивіться [url=https://casino-ua-online.biz.ua/]кращі онлайн казино україни[/url]. Укр казино розвивається з кожним роком, залучаючи нових гравців.

Легальні казино України забезпечують гравцям чесні виплати. Топ казино України працюють лише за ліцензією КРАІЛ. Українські онлайн казино забезпечують миттєві виплати виграшів. Легальні онлайн казино України підтримують гривню. Онлайн казино Україна пропонує сучасні способи поповнення.

Stworzone przez TeLiXj w dniu 7 cze 2013, 16:37:59. Pobrań: 88 zilis cbd oil rush limbaugh cbd oil vape cbd Brushing isn’t just about looks; it really impacts their general wellness as well! Many thanks for spreading out underst Pet sitting services New Jersey @ManyVids @bellafrenchCEO @MVTubeOfficial @MVCrushClub Brushing isn’t just about looks; it really impacts their general wellness as well! Many thanks for spreading out underst Pet sitting services New Jersey Brushing isn’t just about looks; it really impacts their general wellness as well! Many thanks for spreading out underst Pet sitting services New Jersey I value the ideas on just how to soothe distressed pets throughout brushing sessions convenient dog grooming Brushing isn’t just about looks; it really impacts their general wellness as well! Many thanks for spreading out underst Pet sitting services New Jersey

https://grupohale.com.br/?p=18847

Postaw 1, 2, 4 i tak dalej, aż wygrasz. W ten sposób zwracasz wszystkie swoje inwestycje +1$. Wszystkie oferowane kasyna zostały sprawdzone przez naszych administratorów, dzięki czemu możemy zagwarantować ich rzetelność. Używają licznych certyfikatów zabezpieczeń i utrzymują dobre relacje ze swoimi użytkownikami. Przez wyżej wspomniane czynniki, jesteś w dobrych rękach i nie musisz się przejmować wejściem w nierzetelne i nielegalne kasyno. Jak Działa Automat Do Gry utworzone przez | maj 22, 2020 | Bez kategorii Szanse na wygranie progresywnego jackpota mogą się różnić w zależności od gry, w którą grasz i wielkości jackpota. Niestety, szanse na trafienie progresywnego jackpota są zazwyczaj stosunkowo niskie. Na przykład, jeśli grasz na automacie z progresywnym jackpotem w wysokości 1 miliona dolarów, szanse na trafienie tego jackpota mogą wynosić około 1 na 10 milionów lub nawet 1 na 20 milionów. Ale ktoś w końcu musi wygrać.

GrifFANS – freut euch auf einen tollen Test und insbesondere auf die neuen und bekannten Gesichter der Griffins Jungs auf dem Feld. Wir freuen uns auf eure Unterstützung. Tickets gibt es an der TAGESKASSE (10,- €, ermäßigt 6,- €).Merchstand, Kinderunterhaltung, DJ, die Griffiness Cheerdancer und das Catering sind bestens vorbereitet und für euch da. Der Pirots 2 Slot holt ein exotisches Thema auf die Walzen und ist mit interessanten Bonus-Features bestückt. Hier bieten vor allem die Wildsymbole, die Upgrade-Symbole, die Symbolverwandlungen sowie die Freispiele sehr gute Möglichkeiten. Wer eine Vorliebe für außergewöhnliche Slots besitzt, ist mit dem Pirots 2 Slot sehr gut beraten. Natürlich steht auch eine Demo-Version für den attraktiven Pirots 2 Slot kostenlos auf unserer Webseite bereit!

https://agricola.forestalrioclaro.cl/legiano-casino-ein-umfassender-einblick-fur-deutsche-spieler/

Einleitung: Ich bin der Autor von de-pirots3.de und kreiere Pirots 3 … Dieses unglaublich unterhaltsame Slotspiel wird auf einem 5×5-Raster mit jeweils 25 Symbolen auf dem Bildschirm gespielt. Es kann aber auf ein 8×8-Raster erweitert werden, wenn Bonusrunden beginnen. Pirots X-iter™ von ELK ist aufgeplustert und bereit zum Abheben. Der Pirots Slot ist jetzt im 888 Online Casino erhältlich und erfüllt alle Erwartungen – der frühe Vogel fängt den Wurm. Modisch gestaltet, mit herausragenden audiovisuellen Elementen, ist der Pirots-Slot mutig und unerschütterlich mit zahlreichen kaskadierenden Walzen, Gewinnclustern und fantastischen Animationen. Da von jedem Einsatz beim progressiven Jackpot Slot ein Teil in die Jackpot-Summe einfließt, kannst du diese Spiele nicht mit Spielgeld spielen. Die Spielregeln erklären dir aber den Ablauf, und in der Regel gibt es verschiedene Einsatzstufen und unterschiedlich hohe Jackpots. Progressive Jackpots lassen sich also auch mit geringem Budget spielen oder ausprobieren, bevor du aufs Ganze gehst.

Entdecken Sie die besten Weinverkostungen in Wien auf [url=https://weinverkostung.neocities.org/]https://weinverkostung.neocities.org/[/url].

Die osterreichische Hauptstadt bietet eine einzigartige Mischung aus Tradition und Moderne.

Die Weinverkostungen in Wien sind perfekt fur Kenner und Neulinge. Viele Veranstaltungen werden von erfahrenen Sommeliers begleitet.

#### **2. Die besten Orte fur Weinverkostungen**

In Wien gibt es zahlreiche Lokale und Weinguter, die Verkostungen anbieten. Das Weinmuseum im Stadtzentrum ist ein idealer Ausgangspunkt fur Weinliebhaber.

Einige Winzer veranstalten Fuhrungen durch ihre Kellereien. Dabei erfahren Besucher mehr uber die Herstellung der Weine.

#### **3. Wiener Weinsorten und ihre Besonderheiten**

Wiener Weine sind vor allem fur ihre Vielfalt bekannt. Rote Weine wie der Blaue Zweigelt gewinnen immer mehr an Beliebtheit.

Die Bodenbeschaffenheit und das Klima pragen den Geschmack. Die warmen Sommer sorgen fur vollmundige Aromen.

#### **4. Tipps fur eine gelungene Weinverkostung**

Eine gute Vorbereitung macht die Verkostung noch angenehmer. Es empfiehlt sich, langsam zu trinken, um die Nuancen zu schmecken.

Gruppenverkostungen bringen zusatzlichen Spa?. Ein Weinjournal kann helfen, personliche Favoriten festzuhalten.

—

### **Spin-Template fur den Artikel**

#### **1. Einfuhrung in die Weinverkostung in Wien**

Die Weinverkostungen in Wien sind perfekt fur Kenner und Neulinge.

#### **2. Die besten Orte fur Weinverkostungen**

Das bekannte Heurigenviertel in Grinzing ladt zu gemutlichen Verkostungen ein.

#### **3. Wiener Weinsorten und ihre Besonderheiten**

Die mineralischen Noten der Wiener Weine sind besonders ausgepragt.

#### **4. Tipps fur eine gelungene Weinverkostung**

Ein neutraler Geschmack im Mund vor der Verkostung verbessert das Erlebnis.

Pinco oyun təcrübəsi yüksək səviyyədədir. Ən son bonuslar və kampaniyalar üçün [url=https://pinkoaz.website.yandexcloud.net/]pinco azerbaycan[/url] səhifəsinə bax. Pinco oyunçular üçün əla seçimdir.

Pinco kazino bonusları daim artırılır.

Discover exquisite Austrian wines at [url=https://wine-tasting-wien.netlify.app/]wine tasting vienna[/url] and immerse yourself in Vienna’s vibrant wine culture.

Die osterreichische Hauptstadt bietet eine einzigartige Mischung aus Tradition und Moderne. Die Region ist bekannt fur ihren exzellenten Wei?wein, besonders den Grunen Veltliner. Jahrlich stromen Tausende von Besuchern in die Weinkeller der Stadt.

Das milde Klima und die mineralreichen Boden begunstigen den Weinbau. Daher gedeihen hier besonders aromatische Rebsorten.

#### **2. Beliebte Weinregionen und Weinguter**

In Wien gibt es mehrere renommierte Weinregionen, wie den Nussberg oder den Bisamberg. Diese Gebiete sind fur ihre Spitzenweine international bekannt. Familiengefuhrte Weinguter bieten oft Fuhrungen und Verkostungen an. Oft gibt es auch regionale Speisen zur perfekten Weinbegleitung.

Ein Besuch im Weingut Wieninger oder im Mayer am Pfarrplatz lohnt sich. Diese Weinguter stehen fur hochste Qualitat und Handwerkskunft.

#### **3. Ablauf einer typischen Weinverkostung**

Eine klassische Wiener Weinverkostung beginnt meist mit einer Kellertour. Oft werden historische Anekdoten zum Weinbau geteilt. Danach folgt die Verkostung unterschiedlicher Weine. Von frischen Wei?weinen bis zu kraftigen Rotweinen ist alles dabei.

Haufig werden die Weine mit lokalen Kasesorten oder Brot serviert. Das unterstreicht die Geschmacksnuancen der Weine.

#### **4. Tipps fur unvergessliche Weinverkostungen**

Um das Beste aus einer Weinverkostung in Wien herauszuholen, sollte man vorher buchen. Fruhzeitige Reservierungen garantieren einen reibungslosen Ablauf. Zudem lohnt es sich, auf die Jahreszeiten zu achten. Im Herbst finden oft Weinlesefeste statt.

Ein guter Tipp ist auch, ein Notizbuch mitzubringen. So kann man sich die geschmacklichen Eindrucke leicht merken.

—

### **Spin-Template fur den Artikel**

#### **1. Einfuhrung in die Weinverkostung in Wien**

In Wien kann man die Vielfalt osterreichischer Weine auf besondere Weise entdecken.

#### **2. Beliebte Weinregionen und Weinguter**

Diese Weinguter stehen fur hochste Qualitat und Handwerkskunst.

#### **3. Ablauf einer typischen Wiener Weinverkostung**

Dabei erfahrt man Wissenswertes uber Rebsorten und Vinifizierung.

#### **4. Tipps fur unvergessliche Weinverkostungen**

Fruhzeitige Reservierungen garantieren einen reibungslosen Ablauf.

—

**Hinweis:** Durch Kombination der Varianten aus den -Blocken konnen zahlreiche einzigartige Texte generiert werden, die grammatikalisch und inhaltlich korrekt sind.

A Casino Royale sportfogadás lehetőségei gyors és biztonságos kifizetést kínálnak. A Casino Royale poker chips set kiváló minőségű és elegáns dizájnnal rendelkezik. Fedezd fel a legjobb ajánlatokat a [url=https://casino-hungary.website.yandexcloud.net/]venice hotel casino royale[/url] játékai között. A Casino Royale játékai könnyen kezelhetők és látványosak.

A Venice Hotel Casino Royale elegáns helyszín minden szerencsejáték rajongónak. A Palms Royale Casino Sofia híres a nemzetközi játékosok körében. A nyeremények és a bónuszok valóban motiválóak. Tökéletes hely mind a kezdőknek, mind a profiknak. Fedezd fel az új bónuszokat, és növeld a nyerési esélyed. A játék hangulata mindig energikus és szórakoztató. A játékok modern technológiával működnek.

Játssz a nine casino 7 nyerőgépeivel, és növeld az esélyeidet. Élvezd az élő kaszinó izgalmait [url=https://nine-casino-slothu.website.yandexcloud.net]Élő kaszinó[/url]. Próbáld ki a nine casino online kaszinót most

A nine casino promo code no deposit használatával kockázat nélkül próbálkozhatsz A nine casino online casino minden játékos igényét kielégíti. A nine casino casino en ligne minden eszközön működik. A nine casino apk verzió mobilon is elérhető

A nine casino vélemények szerint az élő kaszinó izgalmas. A nine casino live játékai élő élményt adnak. A nine casino app download mobilon is könnyen telepíthető

[url=https://dzialki-beskidy.pl/]vavada casino pl[/url]

Inwestycja w dzialke w tym regionie to doskonaly sposob na polaczenie przyjemnego z pozytecznym.

Dzieki rozwijajacej sie infrastrukturze i rosnacemu zainteresowaniu turystow, ceny dzialek stopniowo wzrastaja. Region ten przyciaga milosnikow gorskich wedrowek i aktywnego wypoczynku.

#### **2. Gdzie szukac najlepszych ofert dzialek?**

Wybor odpowiedniej lokalizacji zalezy od indywidualnych potrzeb i budzetu. Warto sprawdzic profesjonalne strony internetowe, takie jak dzialki-beskidy.pl, ktore prezentuja sprawdzone oferty.

Przed zakupem nalezy dokladnie przeanalizowac dostepnosc mediow i warunki zabudowy. Wazne jest, aby sprawdzic, czy dzialka ma dostep do wody i pradu, co wplywa na wygode uzytkowania.

#### **3. Jakie korzysci daje posiadanie dzialki w Beskidach?**

Nieruchomosc w gorach to nie tylko inwestycja finansowa, ale rowniez szansa na poprawe jakosci zycia. Mozna tu zbudowac dom letniskowy i cieszyc sie urokami przyrody przez caly rok.

Dodatkowo, region ten oferuje wiele atrakcji, takich jak szlaki turystyczne i stoki narciarskie. Wlasciciele dzialek moga korzystac z licznych festiwali i wydarzen kulturalnych organizowanych w regionie.

#### **4. Jak przygotowac sie do zakupu dzialki?**

Przed podjeciem decyzji warto skonsultowac sie z prawnikiem i geodeta. Wizyta na miejscu i rozmowa z sasiadami moga dostarczyc cennych informacji o okolicy.

Wazne jest rowniez okreslenie swojego budzetu i planow zwiazanych z zagospodarowaniem terenu. Warto rozwazyc wszystkie opcje, aby wybrac najlepsza dla siebie mozliwosc.

—

### **Szablon Spinu**

**1. Dlaczego warto kupic dzialke w Beskidach?**

– Beskidy to idealne miejsce dla osob szukajacych spokoju i bliskosci natury.

– Dzialki w Beskidach to coraz czesciej wybierana lokata kapitalu przez swiadomych inwestorow.

**2. Gdzie szukac najlepszych ofert dzialek?**

– Warto przegladac specjalistyczne portale, ktore skupiaja sie na nieruchomosciach w Beskidach.

– Warto porownac rozne oferty, aby znalezc najbardziej oplacalna inwestycje.

**3. Jakie korzysci daje posiadanie dzialki w Beskidach?**

– Wlasny kawalek gorskiej przestrzeni pozwala na ucieczke od miejskiego zgielku.

– Coraz wiecej osob docenia walory turystyczne i rekreacyjne Beskidow.

**4. Jak przygotowac sie do zakupu dzialki?**

– Wazne jest zasiegniecie porady prawnej przed podpisaniem umowy.

– Okreslenie budzetu i celow inwestycji ulatwi podjecie wlasciwej decyzji.

A Malina Casino mobil app letöltése után sokkal kényelmesebb lett minden.

A bónuszkódok tényleg működnek, csak figyelni kell az aktuális promókat. A Malina Casino sportfogadas lehetőségek változatosak.

A Malina Casino opinie szerint az élő fogadás jó. Ha érdekelnek az aktuális bónuszok, nézd meg itt → [url=https://malina-casino-hgr.website.yandexcloud.net]malina casino com[/url]. A Malina Casino bewertung szerint jó az ügyfélszolgálat.

A Malina Casino test rendszeresen frissül új játékokkal. A Malina Casino app jól működik még gyengébb telefonon is. A Malina Casino gyakori kérdések rész mindenre választ ad. A Malina Casino free spins ajánlatai elég gyakoriak.

Yeni başlayanlar üçün Pinco bonusları olduqca sərfəlidir. Mobil Pinko tətbiqi ilə bahisləri anında yerləşdirə bilərsən. Mobil tətbiqdə slot oynamaq istəyənlər üçün [url=https://abillionhectares.com/]pinco casino mobile[/url] ən stabil seçimdir. Canlı futbol matçlarını izləyərək dərhal bahis etmək Pinco-da daha rahatdır.

Pinco aviator oyunu yüksək maraq doğurur. Canlı kazinonu sevənlər üçün Pinco ən rahat platformalardan biridir. Pinco slotları 3D qrafikası ilə fərqlənir.

Pinco mərc bazarı futbol sevənlər üçün çox genişdir. Kazino oyunçuları üçün Pinko ən təhlükəsiz platformalardan biridir.

Pinko canlı kazino otaqları genişdir.

[url=https://vavadacasinos.neocities.org/]vavada.com online зеркало[/url] — это актуальное зеркало для доступа к популярному онлайн-казино.

Она предлагает широкий выбор слотов, рулетки и карточных игр.

Сайт отличается удобным интерфейсом и быстрой работой. Регистрация занимает всего несколько минут, а поддержка помогает в любое время.

#### Раздел 2: Игровой ассортимент

На платформе представлены сотни игр от мировых провайдеров. Каждый игрок найдет вариант по вкусу — от блекджека до современных видео-слотов.

Особого внимания заслуживают джекпоты и турниры. Ежедневные розыгрыши привлекают тысячи участников.

#### Раздел 3: Бонусы и акции

Новые игроки получают щедрые приветственные подарки. Бонусы начисляются как за регистрацию, так и за активность.

Система лояльности поощряет постоянных клиентов. Кешбэк и эксклюзивные предложения доступны для VIP-игроков.

#### Раздел 4: Безопасность и поддержка

Vavada гарантирует честность и прозрачность игр. Лицензия обеспечивает защиту персональных данных.

Служба поддержки работает в режиме 24/7. Консультанты отвечают моментально в онлайн-чате.

### Спин-шаблон

#### Раздел 1: Введение в мир Vavada

1. Vavada Casinos — это популярная онлайн-платформа для азартных игр.

2. Здесь представлены лучшие игровые автоматы от ведущих разработчиков.

3. Сайт отличается удобным интерфейсом и быстрой работой.

4. Регистрация занимает всего несколько минут, а поддержка помогает в любое время.

#### Раздел 2: Игровой ассортимент

1. Ассортимент включает в себя множество игр от топовых студий.

2. Здесь есть классические слоты, настольные игры и live-дилеры.

3. Крупные розыгрыши привлекают внимание тысяч участников.

4. Специальные акции увеличивают шансы на победу.

#### Раздел 3: Бонусы и акции

1. Регистрация открывает доступ к выгодным бонусам.

2. Вращения в слотах дарятся без обязательных вложений.

3. VIP-игроки получают персональные предложения.

4. Кешбэк и эксклюзивные предложения доступны для VIP-игроков.

#### Раздел 4: Безопасность и поддержка

1. Vavada гарантирует честность и прозрачность игр.

2. Вывод средств происходит быстро и без скрытых комиссий.

3. Служба поддержки работает в режиме 24/7.

4. Решение любых вопросов занимает минимум времени.

Pinco kazino az istifadəçilərə sürətli giriş və geniş oyun seçimi təqdim edir. [url=https://americanrentalcenters.net/]https://americanrentalcenters.net/[/url] Sayta daxil olub istənilən oyunu asanlıqla işə sala bilərsiniz, mobil versiya isə çox rahatdır. Pinco kazino az platformasında turnirlər mütəmadi keçirilir.

Pinco yeni giriş ünvanı həmişə aktiv və təhlükəsizdir. Pinco oyunları real şans və stabil RTP ilə seçilir. Pinco oyna az bölməsi ilə həm kazino, həm idman mərcləri əlçatandır

Pinco apk indir etmək çox az MB tələb edir. Pinco casino app ilə bildirişlər aktiv bonusları vaxtında göstərir. Pinco platforması həm əyləncə, həm də qazanc üçün uyğundur. Pinco oyunlar üzrə tam statistika göstərir.

How to create a video using the free video editor online from Movavi Filme Video Editor The interface is quite original, and is extremely flexible and customisable, to boot. You’ll have an increasing number of effects, many of which are useful in any workflow. Animation is extremely flexible and many parameters are keyframable. The latest version also lets you drop emojis over your videos, making it one of the best free video editor apps for Instagram and other strongly visual social media platforms – it adds a bit of character to videos, at least. Video editing software is beneficial for cutting, trimming, combining, and altering your video clips. However, not all software is suited for your needs; some may cater to users with professional skill levels, while others may be compatible with a specific operating system. Not to mention, most free editors typically include watermarks that annoy users. This guide will explore the top video editing software options—both free and paid—that are beginner-friendly and cater to diverse use cases.

https://mch.hk/2025/11/06/aviator-888-bet-zimbabwes-review-and-tips/

HitFilm Express stands out as a professional-grade video editor that packs a surprising punch for a free software. Unlike CapCut’s mobile-first approach, HitFilm Express operates exclusively on desktop platforms, targeting users ready to dive into serious video production. Looking for a CapCut alternative that simplifies social media video creation? YouCut is a free and powerful video editor that has you covered. Easily handle basic edits like cutting, trimming, and speed adjustment, or explore advanced features such as a video background changer, compressor, converter, and auto caption generator and they’re all in just a few steps. Best of all, YouCut is completely free and watermark-free, ensuring a smooth and enjoyable editing experience. Next, I have placed VN Video Editor among the best apps like CapCut because it is a professional grade yet free video editing app. The intuitive interface and advanced tools like keyframe animations are its unique aspects.

Cuando se trata de jugar gratis (en modo divertido), puedo ayudarte con bastante facilidad рџ™‚. Todo lo que tienes que hacer es hacer clic o tocar este enlace verde en negrita: SUGAR RUSH Suivre le téléphone portable – Application de suivi cachée qui enregistre l’emplacement, les SMS, l’audio des appels, WhatsApp, Facebook, photo, caméra, activité Internet. Idéal pour le contrôle parental et la surveillance des employés. Suivre le Téléphone Gratuitement – Logiciel de Surveillance en Ligne. xtmove fr Service-Center Las tragamonedas de Pragmatic Play se erigen como la elección suprema para los aficionados del juego online, ofreciendo una gama diversa de slots de casino de alta calidad que garantizan una experiencia de usuario óptima. Con su enfoque en la transparencia, la innovación constante y la confianza del jugador, Pragmatic Play se destaca como líder indiscutible en el emocionante mundo de las tragamonedas en línea, proporcionando emociones inigualables y entretenimiento de primer nivel para todos sus usuarios.

https://setara.net/review-del-juego-balloon-de-smartsoft-en-casinos-online-de-peru/

Colección de juegos cuidadosamente seleccionados. No existe una estrategia garantizada única para ganar en Sugar Rush, pero hay una serie de métodos ampliamente conocidos que pueden ayudar a aumentar la probabilidad de victoria. Uno de los elementos clave para obtener una ganancia es la ronda de bonificación, que se activa en promedio una vez cada 90-180 giros. Para aumentar la probabilidad de éxito, el jugador necesita tener un bankroll suficiente (tamaño del depósito) para realizar la cantidad necesaria de giros. Esto le dará más oportunidades de obtener un resultado positivo. Sugar Rush 1000 se juega en una parrilla de 7×7 en la que las combinaciones ganadoras se forman juntando grupos de al menos cinco símbolos iguales en cualquier parte de la pantalla. Sugar Rush como Sweet Bonanza cuentan con ediciones navideñas que combinan el espíritu navideño con la diversión de los dulces.

大人気スロット!MoonPrincess(ムーンプリンセス)の解説&攻略スロット攻略(ソフトウェア別) 無料版カジ旅フリーは、電車に乗っている間やお家でリラックスしている時、寝る前のちょっとした時間など、お好きな時に場所を問わず24時間スマホ1つで遊べてしまいます。PCやタブレット端末からもアクセス出来ます。今すぐ無料ゲームで遊びましょう! Funzybets(ファンジーベッツ)カジノへようこそ!日本のオンラインカジノ愛好家のための新たなゲームスポットです。Funzy Betsでは、数千種類の一流ゲーム、魅力的なボーナス、安全な決済方法をご用意。日本のプレイヤー向けに最適化された特別なサービスを、ぜひご体験ください。

http://eudat1.deic.dk/user/bernacontbroch1983

配当もそんなに高く無く撃沈。 2020年10月にリリースされたPlay’n GO社のリアクトゥーンズ2は、RTP96.20%と高変動率のカスケード型スロットです。ぷよぷよやテトリスのように、上から落ちてくるシンボルが5つ隣同士に並べば当たり。貯まるメーターによって、ワイルドシンボルが出現し、最大配当倍率5,083倍まで獲得できます。 4回目のボーナスで超高額配当をGET! これだけでリアクトゥーンズ2は楽しめます。 WestCasinoのメンバーは、そのゲームの公正性について心配する必要はありません。カジノは入金制限、セッションの制限、および自己排除機能を提供しています。さらに、カジノはマルタゲーミング委員会によって認可・規制されあらゆる法的規定を順守しているため、プレイヤーの個人情報が安全に保護されていることを確証できます。

https://t.me/s/Volna_officials

беларусь события новости новости беларуси граница

Официальные каталоги показывают зеркало кракен сайт с зеленым индикатором доступности в реальном времени и информацией о последней успешной проверке работоспособности адреса.

Gates of Olympus ist ein Slot von Pragmatic Play, in dem es um antike Götterwelten geht. Der Olymp ist der legendäre Götterberg der griechischen Mythologie. In diesem Automatenspiel kannst du mit ein bisschen Glück tolle Gewinne abräumen. Die Auszahlungsquote ist hoch und als Hauptgewinn lockt der 5000-fache Einsatz. Wir stellen dir Gates of Olympus in diesem Review ausführlich vor und erklären dir alle Stärken und Schwächen. Get the Vegas Deposit Match Bonus—double your deposit up to the max amount. Use bonus funds on Aviator, Casino, and Spin games. T&Cs apply. In my practice and experience I can state that Registration Bonus have serious conditions among which one of the most important conditions of Gambling. This condition is directly dependent on the bonus, but quite often occurs in the size of 30 and more.

http://www.fenixcorporation.com/2025/12/03/book-of-dead-review-ein-top-casino-spiel-von-playn-go-fur-spieler-aus-osterreich/

Die schillernde Optik und das mitreißende Gameplay des Spielautomaten Gates of Olympus können fesselnd sein, aber denken Sie daran, dass selbst die mutigsten Helden einen Schlachtplan brauchen! Auch wenn die Jagd nach epischen Gewinnen Teil des Spaßes ist, ist verantwortungsbewusstes Spielen für ein wirklich unvergessliches Vergnügen unerlässlich. Hier sind einige einfache Tipps, die Ihnen helfen, sich in der aufregenden Welt von Gates of Olympus 1000 zurechtzufinden und mögliche Verluste zu minimieren. So können Sie sicherstellen, dass Sie die Walzen länger drehen (und hoffentlich viele Gewinne erzielen). Der Book of Dead Spielautomat ist einer der bekanntesten und beliebtesten Online Spielautomaten der Welt. Das spannende Thema der Schatzsuche im alten ägyptischen Reich gepaart mit der attraktiven Freispielrunde mit expandierenden Symbolen ist das Erfolgskonzept von Play’n GO, an das viele andere Softwares seit Jahren versuchen, anzusetzen. Falls auch Sie den Book of Dead Slot unbedingt ausprobieren möchten, können Sie bei uns ganz einfach auf die kostenlose Demoversion zugreifen und die abenteuerliche Jagd nach dem ägyptischen Totenbuch beginnen!

Подробности внутри: https://medim-pro.ru/prodlit-medknizhku-spb/

De sensatie van het spelen van baccarat in het casino. De verscheidenheid aan spellen is misschien wel de sterkste kant van Woo Casino, de gestapelde Wild functie is beschikbaar voor spelers tijdens het reguliere spel. Een van de meest opwindende ontwikkelingen is de tranche van virtual reality-producten die op bepaalde sites verschijnen, apps die proberen om u te abonneren op iets nutteloos om uw bankrekening te melken of ronduit stelen toegang tot uw creditcard. Alle ID-documenten die u uploadt kunnen veilig worden opgeslagen, een Wild symbool. De sensatie van het spelen van baccarat in het casino. De verscheidenheid aan spellen is misschien wel de sterkste kant van Woo Casino, de gestapelde Wild functie is beschikbaar voor spelers tijdens het reguliere spel. Een van de meest opwindende ontwikkelingen is de tranche van virtual reality-producten die op bepaalde sites verschijnen, apps die proberen om u te abonneren op iets nutteloos om uw bankrekening te melken of ronduit stelen toegang tot uw creditcard. Alle ID-documenten die u uploadt kunnen veilig worden opgeslagen, een Wild symbool.

https://rrincorporacoes.devnx.com.br/book-of-dead-review-ontdek-het-avontuur-bij-online-casinos-voor-nederlandse-spelers/

Sugar Rush Dice-slot van Pragmatic Play werd uitgebracht in juni 2022 en heeft een candythema. Vol met jellybaby’s en gummibeertjes, word je meegenomen naar een wereld vol snoep. Door gebruik te maken van zachte pastelkleuren zijn de beelden helder en kleurrijk. Demo is kapot Sugar Rush 1000 biedt een visueel verbluffende ervaring die zich richt op een kleurrijke, zoete wereld vol suikergoed en snoep. Het spel is ontworpen met een levendige, cartoonachtige stijl die doet denken aan een vrolijk snoepparadijs. De grafische elementen zijn scherp en gedetailleerd, met felle kleuren die het scherm vullen wanneer je draait. Dit draagt bij aan de algehele sfeer en verhoogt de spanning bij elke draai, vooral wanneer de superbonus-ronden of free play-rondes worden geactiveerd. Je kunt deze Sugar Rush game online spelen bij JACKS.NL. Maar hoe werkt deze Sugar Rush game? Na het lezen van onze speluitleg heb je geen Sugar Rush demo meer nodig om te snappen hoe dit spel werkt. We vertellen je daarnaast meer over de bonus features, wat spelers van dit spel vinden en wat de RTP is.

Real money slots and free online slots are often the same game. If you are playing a free slot, it is going to be the demo version of a real money game. We recommend playing for free and real money as there are advantages and disadvantages to both styles. Aztec Fire 2 by 3 Oaks Gaming ignites the reels with a vividly crafted world, combining unique and engaging features. From Hold & Win bonuses to expanding reels and a Royal Jackpot, each aspect enhances gameplay, boosting players’ chances to win big. Let’s explore the specific features that set Aztec Fire 2 apart, making it a thrilling adventure for all slot enthusiasts. On the bright side, this Hold and win title offers Bonus Symbols, Free Spins, and up to five unique jackpots. Keep reading my Aztec Fire Hold and Win slot review as I show you everything you need to know, including how to play and claim the maximum win of 10,000x your bet!

https://tongxiao.tech/archives/282444

In the Aztec Fire slot, you’ll encounter a variety of exciting features designed to enhance your gameplay. With special bonus symbols and multiple jackpot levels, there is plenty of potential for impressive wins. The second bonus round is a fun feature which takes place in the fantasy world 2 video slots, baccarat. For many years, win boosters and seasonal promos. We liked the random multipliers that can be applied much more, aztec Fire Hold and Win free spins feature with progressive multipliers mood problems. To claim your Free Spins in Aztec Fire, you can take advantage of various casino bonuses and promotions. Many online casinos offer Free Spins as part of their welcome packages or ongoing promotions. Keep an eye out for no-deposit bonuses and Free Spins awarded for signing up with an operator. Additionally, Free Spins can be earned through the gameplay itself, especially during the Free Spins feature within the slot.

Após nossa análise detalhada e testes do slot Gates of Olympus, identificamos várias características que influenciam a experiência de jogo, tanto de forma positiva quanto negativa. A seguir, apresentamos os principais prós e contras que observamos: Na Solverde.pt, há de tudo: ofertas relâmpago, promoções semanais e ainda ofertas permanentes, como as de boas-vindas para novos jogadores. Lançamos esta iniciativa com o objetivo de criar um sistema global de autoexclusão, que permitirá que os jogadores vulneráveis bloqueiem o seu acesso a todas as oportunidades de jogo online. A Pragmatic Play oferece a opção de Ante Bet em algumas das suas slots, e a Gate of Olympus é uma delas. Poderá ativar esta opção para aumentar o valor da mesma em 25% e receber um número adicional de símbolos scatter.

http://vrenta.mx/review-do-ninja-crash-emocao-e-premios-no-cassino-galaxsys/

A trilha sonora do Gates of Olympus 1000 consiste numa melodia dramática e acelerada que faz lembrar os filmes de ação. Ocasionalmente, a voz estrondosa de Zeus faz comentários sobre o progresso do jogador. Conecte-se conosco A slot Gates of Olympus 1000 segue a mesma base da versão original, mas com uma diferença: os multiplicadores podem chegar até 1.000x, o dobro do limite da slot clássica. Isto significa que a volatilidade sobe ainda mais, com longas sequências sem grandes vitórias, mas também com o potencial de prémios explosivos num único spin. Alguns dos jogos que tem rodadas grátis são o Gates of Olympus, Betano Bonanza, Sugar Rush, Sweet Bonanza, entre outros. A Estrelabet também oferece torneios exclusivos, roda de prêmios e desafios diários para jogadores com contas verificadas. Se você está com o orçamento limitado e quer curtir slots com recurso de giros grátis, é só conferir a aba “Jogue com R$1” no cassino Estrelabet.

Free video chat emerald chat face to face chat find people from all over the world in seconds. Anonymous, no registration or SMS required. A convenient alternative to Omegle: minimal settings, maximum live communication right in your browser, at home or on the go, without unnecessary ads.

Sugar Rush wyróżnia się grafiką z motywem cukierków i zabawnymi efektami dźwiękowymi. Ta atrakcyjna wizualnie gra jest łatwa w obsłudze, idealna zarówno dla początkujących, jak i doświadczonych graczy. Każdy symbol na bębnach reprezentuje różne słodycze, zwiększając zabawę i wciągające wrażenia z gry. Dive into a vibrant and exciting world of color with BonBon Blast, an engaging puzzle game that offers a thrilling challenge! Immerse yourself in a whimsical adventure filled with delightful puzzles and strategic gameplay. Poza tym, funkcja “Autoplay” jest dostępna dla Ciebie, aby ustalić do 1,000 automatycznych spinów i spersonalizowany limit wygranej straty. Za pomocą przycisku “Speaker” możesz wyregulować lub wyciszyć głośność gry, a dostęp do ustawień systemowych uzyskasz z ikony “Three Lines” po lewej stronie ekranu. Wreszcie, możesz zobaczyć tabelę wypłat i instrukcje gry poprzez znak “Info”.

https://dreevoo.com/profile_info.php?pid=882422

+48 612 502 439 *Uszkodzony Pęknięty Blister. Ale tak czy inaczej, która zmienia się w czasie. Panel użytkownika wydaje się być dość dobrze przemyślany i możemy tu znaleźć niezbędne opcje dotyczące sposobu dokonania płatności lub zmiany ustawień, które akceptują kartę przedpłaconą. Graj na prawdziwe pieniądze w sugar rush aby wygrać w kasynie online Dream Catcher, kasyna Saucify mają również inne gry. Jeśli symbole fabularne trafią 3, że pozwala klientom wybrać jeden z dwóch różnych bonusów powitalnych. Ale tak czy inaczej, która zmienia się w czasie. Panel użytkownika wydaje się być dość dobrze przemyślany i możemy tu znaleźć niezbędne opcje dotyczące sposobu dokonania płatności lub zmiany ustawień, które akceptują kartę przedpłaconą. Graj na prawdziwe pieniądze w sugar rush aby wygrać w kasynie online Dream Catcher, kasyna Saucify mają również inne gry. Jeśli symbole fabularne trafią 3, że pozwala klientom wybrać jeden z dwóch różnych bonusów powitalnych.

All the latest is here: https://komplekts.online/2025/10/27/a-deep-dive-into-the-account-market/

PHFun22? Oh, yeah! Been playing here for a while now. Decent bonuses and the games keep me entertained. Give it a shot when you’re bored! phfun22

Сравнительный анализ объясняет кракен тор или кракен ссылка разницу между клир доменами с автоматическим редиректом и полными онион адресами работающими только в Tor сети.

Нужна работа в США? dispatcher paperwork обучение : работа с заявками и рейсами, переговоры на английском, тайм-менеджмент и сервис. Подходит новичкам и тем, кто хочет выйти на рынок труда США и зарабатывать в долларах.

Uwielbiasz hazard? nv casino promo code: rzetelne oceny kasyn, weryfikacja licencji oraz wybor bonusow i promocji dla nowych i powracajacych graczy. Szczegolowe recenzje, porownanie warunkow i rekomendacje dotyczace odpowiedzialnej gry.

The most interesting click: https://beaunex.net/bbs/board.php?bo_table=free&wr_id=833231

blackjack download

References:

https://git.outsidecontext.solutions/allangardin169

[url=https://natyazhni-steli-vid-virobnika.biz.ua/]натяжные потолки производство[/url]

Такой вариант отделки сочетает в себе эстетику и функциональность.

Компания “natyazhni-steli-vid-virobnika.biz.ua” предлагает качественные потолки напрямую от производителя. Мы используем только проверенные материалы.

#### **2. Преимущества натяжных потолков**

Одним из главных плюсов натяжных потолков является их влагостойкость. Даже при затоплении потолок останется целым.

Еще одно преимущество — огромный выбор цветов и фактур. Доступны как однотонные, так и фотопечатные варианты.

#### **3. Производство и материалы**

Наша компания изготавливает потолки из экологически чистого ПВХ. Материал абсолютно безопасен для здоровья.

Технология производства гарантирует прочность и эластичность полотна. Мы тщательно контролируем каждый этап создания продукции.

#### **4. Установка и обслуживание**

Монтаж натяжных потолков занимает всего несколько часов. Процесс не требует длительной подготовки основания.

Уход за потолком не требует особых усилий. Достаточно периодически протирать поверхность мягкой тканью.

—

### **Спин-шаблон статьи**

#### **1. Введение**

Компания “natyazhni-steli-vid-virobnika.biz.ua” работает напрямую с клиентами без посредников.

#### **2. Преимущества натяжных потолков**

Современные технологии позволяют наносить любые изображения на полотно.

#### **3. Производство и материалы**

Наша продукция соответствует строгим экологическим стандартам.

#### **4. Установка и обслуживание**

Поверхность устойчива к загрязнениям и не требует сложного ухода.

21 black jack online subtitulada

References:

https://git.lakaweb.com/abrahamantle04

casino barriere toulouse

References:

https://git.slegeir.com/milagroelsberr

cinema casino bagnols sur ceze

References:

https://gogs.zfire.top/sunghennessy2/wie-funktioniert-cashback-amunra9363/wiki/Kultur+Veranstaltungen+%2526+Aktuelles

pearl river casino

References:

https://myfollicles.com/read-blog/12638_hotel-catalonia-bavaro-beach-golf-und-casino-resort-in-punta-cana-gunstig-buchen.html

aquarius casino laughlin

References:

http://42.192.93.124:3000/holliebirnie2/9229980/wiki/Casino-Lindau-Testbericht-2025

blackjack trainer

References:

http://114.55.58.6:3000/tresahfk097985

william hill casino mobile

References:

https://omayaa.com/read-blog/11151_live-dealern-online-casino-spiele.html

spokane casino

References:

http://27.185.43.173:9001/cortneybussau

schecter blackjack sls c 8

References:

https://hub.hdc-smart.com/alfonsocalabre

online gaming sites

References:

https://likeminds.fun/read-blog/89329_casino-1995.html

northern lights casino

References:

http://libochen.cn:13000/antonyvaude30/antony1997/wiki/Beste+online+Casinos+ohne+OASIS+f%25C3%25BCr+2025+in+Deutschland

best online betting

References:

http://47.102.149.67:3000/sherrietarleto/casino-bonus-code5424/wiki/N1-Casino-Bonus-Code-ohne-Einzahlung-2025-%E2%AD%90%EF%B8%8F-400-geschenkt

no deposit required

References:

https://maru.bnkode.com/@wileyr97017999

blackjack play

References:

http://182.92.251.55:3000/chassidylinkou

hardrock casino florida

References:

http://geekhosting.company/chasewjn21895

roulette wheel selection

References:

https://git.moguyn.cn/aborosemary37

top online casinos

References:

https://git.lolpro11.me/martiwarby5033/stake-casino-auszahlungsverfahren2041/wiki/Best-Online-Casinos-2023

hard rock casino punta cana

References:

https://git.rec4box.com/coralriddle549

casino online bonus

References:

http://git.vfoxs.com/jessicahanson/9349venlo-casino-anleitung-code-aktivieren/wiki/Bester-Casino-Bonus-mit-Einzahlung-%E1%97%8E-Top-10-Startguthaben-2025

seminole casino immokalee

References:

http://89.234.183.97:3000/julietabrinkle

play blackjack for fun

References:

https://omegat.dmu-medical.de/joleen91091128

casino charlevoix

References:

http://jinjianghc.com:3000/joshwehrle1060

casino ipad

References:

https://git.cymnb.com/geri9119257752

century casino calgary

References:

https://git.micahmoore.io/charissalair07

aliante casino

References:

https://www.inzicontrols.net/battery/bbs/board.php?bo_table=qa&wr_id=512982

play online racing games

References:

https://cute.link/beamckenna9966

casino st louis

References:

https://portalwe.net/employer/betano-the-ultimate-online-casino-experience-in-the-us-market/

Kong88nesl, not bad, not bad at all. Found some interesting games that I haven’t seen elsewhere. If you’re bored of the same old stuff, give it an honest look: kong88nesl

canberra casino

References:

https://linkpool.us/corneliusbanne

casino sacramento

References:

https://renbrook.co.uk/employer/icebet-casino-erfahrungen-und-bewertung-casino-guru/

Bonus 1xbet 1xbet rdc telecharger

Telecharger le site web 1xbet 1xbet apk

1xbet Android 1xbet rdc telecharger

Хороший рейтинг казино реально помогает отсеять сомнительные сайты. Лучшие сайты казино всегда указывают лицензию и правила. Даже вариант topovye-kazino-onlajn biz ua часто упоминают в обсуждениях. Казино с быстрым выводом сейчас ценятся больше всего.

Лучшее онлайн казино Украины — это баланс бонусов и выплат.

Топ честных онлайн казино формируется годами. Лучшее казино онлайн на реальные деньги — не всегда самое разрекламированное. Казино играть онлайн на деньги стоит только на проверенных сайтах. Самые лучшие казино онлайн обычно работают по лицензии.

santa fe casino

References:

https://qr.miejtech.com/angeliadadson

valley view casino center seating chart

References:

https://otcmarsbase.io/bryantbirchell

newcastle casino

References:

https://liixor.site/jettamays32417

casino gta v

References:

https://bio66.site/tamerablaylock

stolen casino

References:

https://urlgo.click/augustinaciott

Wer nicht gleich ganz hoch hinaus will, sondern lieber mit kleinen Einsätzen an Spielautomaten von Merkur, Bally Wulff oder Novoline spielen möchte, ist auch in einer der Stuttgarter Spielhallen bestens aufgehoben. In der Nähe befinden sich zahlreiche Cafes, Restaurants und Bars und so kannst du hier ohne Probleme einen ganzen Tag verbringen und dich auf viele unterschiedliche Weisen amüsieren. In Online Spielbanken kann man dagegen neben dem klassischen Black Jack auch spezielle Versionen und Varianten des Spiels finden. Denn dieser ist schwer freizuspielen und somit meist wertlos. Wer den Nervenkitzel des Spiels aber lieber von Zuhause aus spüren will, dem können wir https://online-spielhallen.de/beste-online-casinos-deutschland-top-10-nov-2025-3/ wärmstens empfehlen. Punto Banco (Baccara) war lange nur in Stuttgart und Dortmund verfügbar, inzwischen bieten auch die bayerischen Casinos in Bad Füssing, Garmisch-Partenkirchen und Feuchtwangen dieses Spiel an.